It’s Time to Get Organized! Create a financial binder to keep important papers all in one place. The binder is a quick way to help you pay attention to your finances on a regular basis. Keeping files electronically is great, but sometimes it is nice to just grab a binder and flip to the page you need!

We get what seems like a million pieces of paper each year. It is easy to get overwhelmed by the piles of paperwork on the counter. One of my quick go to methods to organize papers is to use three ring binders. There are several products I use and love and I am linking them below, but you can use what you have on hand or keep an eye out for sales.

I put together three ring binders for many areas of my life. Binders are cheap and I buy them whenever I see them on sale. At a yard sale or thrift store they often go for as little as fifty cents each. I mainly use all white binders because I prefer the clean look and can dress them up with a slip-in cover page. You can create binders for many areas such as: health files divided by each person in your house, a binder for pets with all their records, one for each grade level of your children, a family emergency binder, kitchen recipes, warranties and manuals, vacations, and a binder for financial papers. For the financial binder, start with a 1 ½ ”or 2” binder that has a slip in cover page where you can insert a copy of your emergency savings tree printable or your index or any cover page.

In addition to a three-ring binder, I use the tabs numbered 1 to 10 (you can buy tabs in more or less numbered versions). Get these at an office supply store or Amazon. Right now Amazon has a great sale to buy 6 sets for under $10, and once you make this binder, you will want to make other binders! These numbered tabs come with a handy index page that you can write or type on, or use a label maker (I love my brother p-touch label maker, it often goes on sale near Christmas and back-to-school time) But I often just use a spreadsheet to create my own index page. Some examples of categories you might use to label the index page of your tabs are below.

Grab this free printable for the index page above!

If using these tabs for your financial documents binder, below are a few financial papers to place behind each tab. I will be writing about many of these items in the coming months, so if you don’t have them now or know what they are, stay tuned.

Tab 1, a copy of your overall financial net worth statement

Tab 2, a printout of your monthly budget plan

Tab 3, a listing and detail of all your debt and your debt snowball plan

Tab 4, print out copies of your 401K quarterly statements

Tab 5, sign up at ssa.gov for your annual social security report and put the most recent copy in the binder every year

Tab 6, any bank or investment records

Tab 7, a copy of all your insurance policies: Car, Home, Life, etc.

Tab 8, a few of your recent pay stubs, and your most recent year end W-2 statement

Tab 9, is for any important information such as a list of all credit cards, bank information, mortgage information and contact information for all your financial accounts to name a few

Behind tab 10, your most recent credit reports

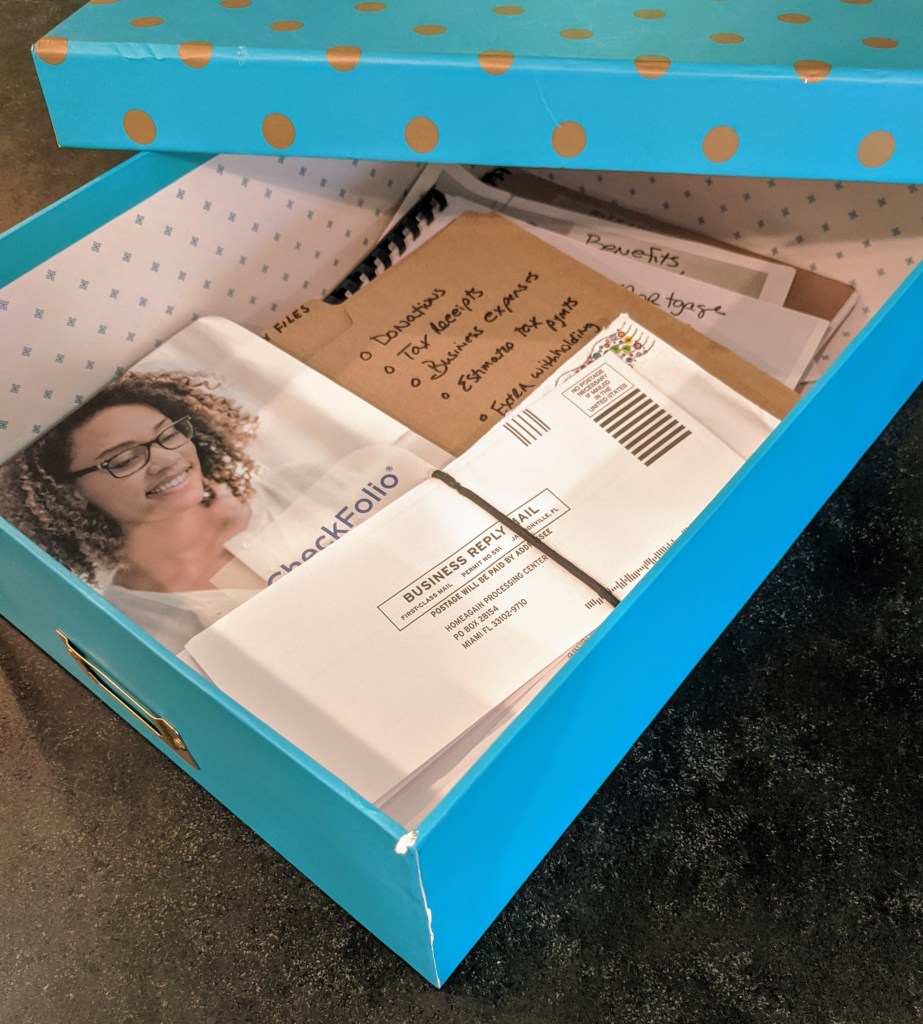

As you make this book, you may have different or additional categories to add based on the financial papers in your box from week one’s post. I have college funds for my children, and I might add a tab for college planning. As your binder gets too thick, transfer some older papers out of the book into an archive binder or start a new separate book. For example, a spinoff binder might be for retirement planning only.

I also like to place a business card sleeve in the front of my binder to slide in any business cards of financial contacts you might have such as a bank manager, an investment broker, a mortgage company, etc. Additionally, I always have a few of these plastic sleeves in case I don’t want to hole punch a paper, or if the paper is a different size than your binder and you need to fold it.

Once you have your binder, tabs, and index sheet, grab a three hole punch, go through your financial records and start placing documents behind the appropriate tab. Make this financial binder work for your personal situation; it will continue to evolve over the years. I like to finish my book off with a label on the spine. Always place your labels on so that when the binder lays flat, you can read the label.

I keep these binders in a dish rack like this one to keep them standing upright, in my home office, or on a nearby bookshelf. You want them to be handy so that you can grab them at a moment’s notice to look up a loan number, see what the debt snowball looks like, or get a phone number for your mortgage company.

Keep any important papers in your financial binder to have them all in one place. It makes for quick and easy access of your finances. As you begin using the financial binder, you look at and pay attention to your finances more often. Keeping files electronically is great, but sometimes it is nice to just grab a binder and flip to what you need!

Disclosure: If you purchase anything from links in this post or other Jump Rope Finances blog posts, I may receive an affiliate commission. However, I only ever mention products I love and would recommend whether I was being compensated or not. Thank you so much for your support of Jump Rope Finances.

If you like this post, please share and subscribe!