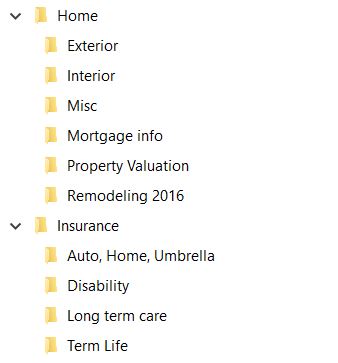

It’s Time to Get Organized! We get what seems like a million pieces of paper each year. It’s easy to get overwhelmed by the piles of paperwork on the counter. And if one of those pieces is a bill or a tax document, sometimes its out of sight, out of mind. It can be easy to accidentally miss the due date.

This post is week four out of six of sharing financial organizing tips. Continue reading to see my method to process bills and paperwork. Although I have automated many of my bills, such as mortgage payment, electric and gas bills, insurance premiums and giving to my church, there are some bills that I still want to see every month like credit card bills and loan statements. This is a photo of my family room bookshelf. You should know; it was much messier before I took the picture!

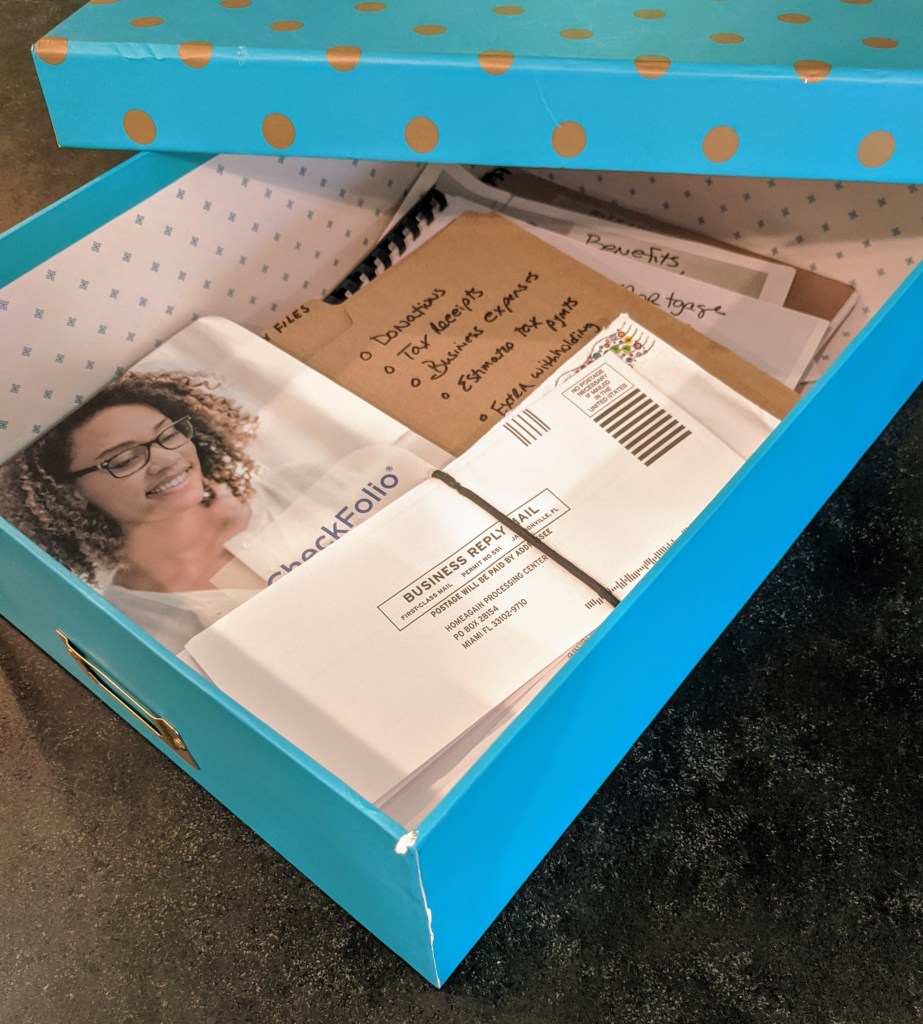

Do you see the black and white box in the middle near the top? It’s actually a file box where I store my incoming bills and important paperwork. When I get bills in the mail, or anything that requires a check (a school form, a tax bill, a registration) and I don’t have time to deal with it, it goes in the box. When I am ready to sit down and pay a bill or fill out the form, I grab the whole box and take it to my kitchen counter.

The box is a Thirty-One Fold N’ File box that I bought at a resale shop. If you want a fold n’ file box like this one, reach out to a thirty-one consultant or check out ebay or Mercari where they sell for about $15 to $25 and come in a variety of patterns. The box size is approximately 12 X 10 X 7. Alternately, you can use pretty rattan basket, or seagrass basket or this gray foldable basket. I also like Marshalls or Target for organizing supplies.

I just toss the bills in the box when received. You could create file folders too, but I found that it is just easier to toss them in and be done with it. The box is simply a temporary holding place for items I need to deal with, to write a check, or complete a form or registration. It is not a long-term storage file. I look through it once or twice a month.

One side of the box is flat and the other has two mesh pockets on the outside.In the pockets I keep blank envelopes, stamps, address labels and a few pens. You could also keep your checkbook here if you still write checks. When I put this on the shelf in my living room, I turn this side towards the wall. If you have a box without the outside pockets, just rubber band the supplies together and toss inside the box with your bills. Or use a plastic pencil case and toss on top. Target has these pencil boxes for about a dollar each.

Although I have automated most of my bills, there are some that I receive monthly because I want to keep track and review them. I have found that if I receive them online, I don’t always look at them with close scrutiny. While online might be fine for the monthly electric bill that doesn’t change much, I do want to see the Target bill and the VISA statement to review my purchases every month. My mortgage payment is made automatically, but I also receive a paper copy in the mail because I like to keep an eye on the outstanding balance. One day we will own our house free and clear!

Once my bills are paid, I toss them into a white Ikea box, in a nearby closet that I’ve turned into a mini office (a future post!).

At one time, I filed everything in file folders by vendor (Phone Company, Electric, Gas, Cable) but that took much time. Next, I tried file folders by month and lumped all together (Jan 2020, Feb 2020 etc.), but I found I rarely went back through them and file folders were jammed in file cabinets. Now I just rubber-band each month’s paid bills together and write the month and year on the top bill with a sharpie, open the box and toss them in. It’s kind of organized in that the last month’s items are always near the top. Since so much is paid automatically, I really don’t have a lot of bills in this box and it usually lasts one or two years before it is full. If I need to reference a paid bill, I pull down the box and shuffle through the rubber banded groups to find the monthly batch. Simple and works for me!

Much like life, things are always changing and what works today, may not work down the road. So, if you try something and it’s not working, find another method.

Disclosure: If you purchase anything from links in this post or any other Jump Rope Finances blog post, I may receive an affiliate commission. However, I only mention products I love and would recommend whether I was being compensated or not. Thank you so much for your support of Jump Rope Finances.

If you liked this post, please share and subscribe.