It’s Time to Get Organized! Keep copies of financial documents and spreadsheets electronically organized on your computer for quick reference. In less than an hour you can set up an organized electronic filing system with this quick guide.

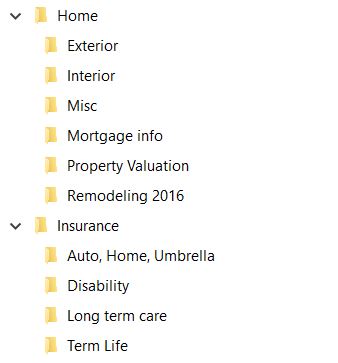

Although I love my financial binder for a quick file reference, I keep many files electronically. On my computer, I have a main master file folder called FINANCES where I have about 12 to 15 subfolders that help organize my financial documents. Every file that is financially oriented goes into one of the subfolders in the master FINANCE folder. Below is a quick snapshot of my FINANCE folder with all the subfolders.

STEP 1: Create a master folder called FINANCES

STEP 2: Create subfolders under the FINANCES folder to store your documents

STEP 3: Move all your financial documents into the appropriate subfolders

Note there are no actual documents in the FINANCES folder – keep everything in a file subfolder within the FINANCES master folder to keep the master folder clean and organized. In making subfolders, you won’t get overwhelmed trying to find files or trying to remember what the document contains without opening each document.

Some examples of items to keep in the subfolders are loan agreements, payment records, monthly or quarterly reports, amortization schedules, maintenance records, purchase records, tax files, etc. In some folders, you can have additional file subfolders. For example, in TAX FILES, there are individual folders for each year.

In the subfolder labeled 2020 store anything that is relevant only to year 2020. For example: monthly bills that are paid electronically, credit card statements, net worth statements, an electronic check register for the year. These are files you may not need to reference on a regular basis beyond year 2020.

On the other hand, if you need to access certain files in the future, such as a home improvement schedule or receipt, you don’t want to be spending time trying to remember which year you purchased or repaired something, so instead put this type of data in the HOME file folder. Within the HOME file, you can have subfolders where you keep information about your mortgage loan, property valuation, interior repairs, exterior repairs, and a master contact listing. For example, we had our roof replaced a few years ago, and keep the related information in a spreadsheet that I can pull up quickly along with the details such as roofer contact name and address, date of replacement, amount paid, warranty information, model, color and shingle type, etc. This spreadsheet is kept in the EXTERIOR folder under the HOME folder. Under the INSURANCE file, you might have subfolders for types of insurance and related information such as policy and contact information stored.

Create organized electronic folders which are applicable to your life. Some other subfolder examples might be Child Care, Scholarships, Social Security, Student Loans, Vacations. For quick access, keep copies of bank statements, financial worth, credit statements, mortgage and car loan information, check register, monthly bills and other self-created spreadsheets electronically organized folders. What about documents that you don’t have electronically, should you consider scanning them into your files? I’ll talk more about this in week 5’s post on Paper files or Scanned files?

Up next week #4: Keeping track of bills and creating a file system for paid bills.

If you like this post, please share and subscribe